This article aggregates published industry data regarding 3D printing including specific filament market figures, whilst also referring to primary research undertaken by Filamentive.

FFF / FDM 3D Printing

https://reprap.org/wiki/File:FFF.png

Fused Deposition Modelling (FDM) or Fused Filament Fabrication (FFF) is the most popular type of 3D printing. FDM / FFF is a process in which a thin plastic wire – known as filament – feeds a 3D printer; the print head melts it and extrudes it onto a build plate to create the desired object, layer-by-layer.

FDM / FFF 3D printing has increased exponentially in recent years due to the rapidly decreasing capital cost of 3D printers, catalysed by the expiry of key patents from 2009.

This particular technology is utilised in the home by hobbyists users, whilst also increasingly implemented in industrial settings, specifically for prototyping work, manufacturing aids, as well as, end-use parts.

UK 3D Printing Market

3DHubs 3D printing trends 2020 report

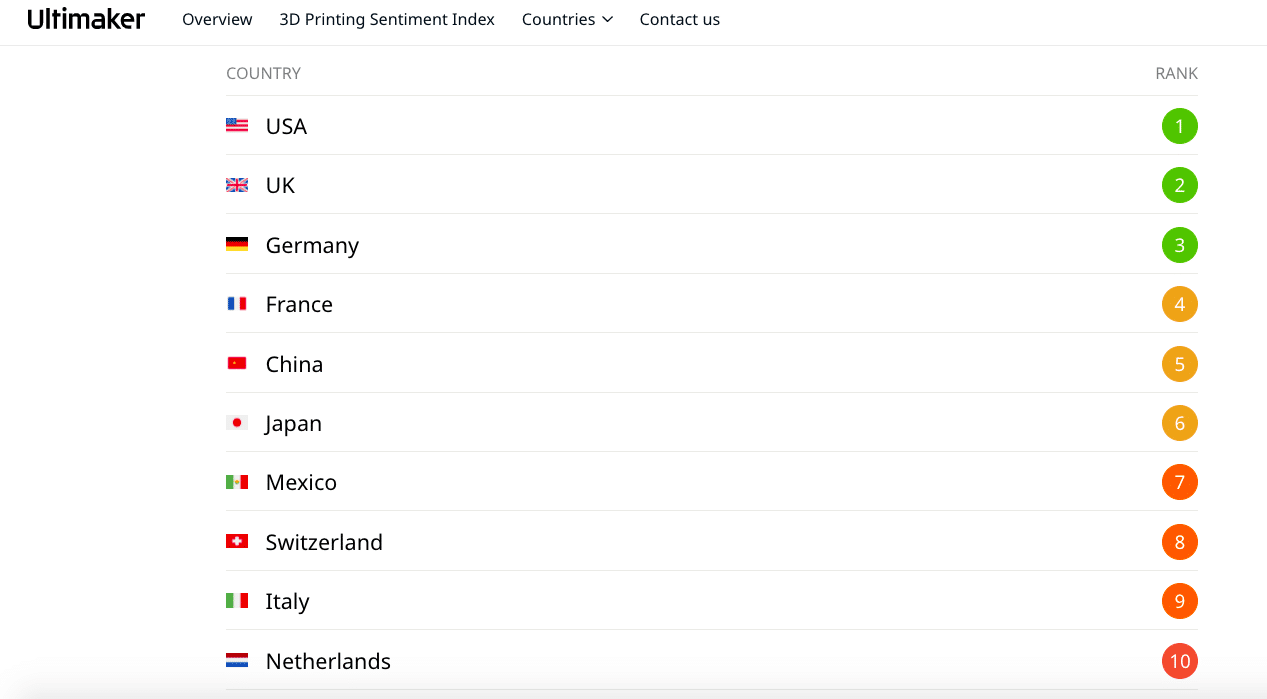

At the time of writing, the UK is listed as 2nd globally the Ultimaker Sentiment Index. Corroborating this, online manufacturing platform, 3DHubs, quantified that the UK is 44% of the total 3D printing demand in Europe. Further 3DHubs data infers the UK could be responsible for up to 20% of global 3D printing volume.

3D Printing Filament Materials

FDM / FFF 3D printing typically relies on thermoplastics as material feedstock. As per 3DHubs 2020 Trends Report, 91% of plastic 3D printing is FDM / FFF, i.e., filament.

There are many types of plastics used for 3D printing filament. This includes: PLA, PETg, ABS, ASA, Nylon, Polycarbonate and composites, such as Carbon Fibre-PETg.

PLA is the most popular 3D printing filament material – Filamentive research found that more than 95% of 3D printing users use PLA. 3D printing users prefer PLA because it’s relatively low-cost and easy to print. As a renewable bioplastic, it is also more environmentally-friendly than traditional, oil-based plastics such as ABS.

UK 3D Printer Filament Usage

Ultimaker Sentiment Index 2019

According to the Ultimaker Sentiment Index, the UK has 168,000 3D printers installed as of 2019. Aggregating with the previous inference that 90% of plastic 3D printing is (plastic) filament based, we can logically assume that in 2019, approx. 151,000 3D printers in the UK were FDM / FFF based.

As per the 3DHubs 2020 Trends Report, 24% is the forecasted average annual growth of the 3D printing market. Using this metric to extrapolate the number of 3D printers installed, it can be inferred that there will be approx. 232,000 3D printers installed in the UK by the end of 2021.

In regards to usage, Filamentive research concluded that the average 3D printer (operator) uses 24 kg of filament annually. Admittedly, most of the 200 respondents were Filamentive customers, a large percentage of which were business users who naturally procure more filament than the average 3D printer user in the UK. Taking a pragmatic approach, it can be assumed the average 3D printer operator in the UK uses 12 kg of filament annually.

Multiplying this by the number of 3D printers in the UK, the estimated 2021 UK 3D printing filament usage can therefore be inferred as approx. 2.8 million kilograms (2800 tonnes).

UK 3D Printer Filament Market Growth

In 2019, Fabbaloo reported that the global filament is expected to grow substantially – specifically, AMECO suggests we may see a rise from the 2017 sales level of US$255M to US$1.2B market value in 2024. Such growth represents a 25% compound annual growth rate.

Earlier in this article, it was inferred that the UK could be up to 20% of global 3D printing; taking a conservative view the UK is only 10% of global 3D printing, this market growth prediction quantifies that the UK 3D printer filament market could be worth US$120M in 2024, or £85.6M adjusted for the live currency exchange rate at the time of writing.

By working backwards from the estimated 2024 value and subtracting 3*25% annual growth, it can be estimated that the 2021 UK 3D Printer Filament Market Value could be £43.8M.

Challenges to the UK 3D Printing Filament

Brexit

Without getting too political, it has become apparent that Brexit has impacted how the UK does business with the rest of the European Union; specifically, due to changes to tax (e.g. VAT) and general import & export procedures. For example, a UK 3D printing user must now pay UK import VAT at 20% if they wish to buy filament from an EU-based supplier, but may also be liable for ancillary fees charged by the courier / customs authorities. A specific example of this is Prusa Research, who initially stopped sending orders to the UK because of the disruption. Conversely, it’s pragmatic to note that the challenge of importing filament from the EU may also be an opportunity for UK extrusion companies to onshore manufacturing of 3D printer filament.

PLA Shortage

Due to a huge increase in demand for sustainable alternatives to regular plastic, there is currently a worldwide PLA shortage. This is because demand for PLA in major industries has considerably increased in recent months – leading to supply shortage and subsequent price increase. This is a potentially significant challenge for the UK 3D printing filament market because as said previously, more than 95% of 3D printing users use PLA. Should the shortage continue and / or the UK filament market demand exceeds supply, this may detrimentally impact 3D printing users. Such a challenge may actually present an opportunity for (more) recycled PLA filament, or possibly increase the usage of other polymers for 3D printing, such as PETg 3D printer filament.

Waste Management

3D printing is something of a double-edged sword when it comes to waste. Whilst at its core, 3D printing is fundamentally less wasteful than traditional, subtractive manufacturing methods, the use of plastic as a feedstock has the potential to exacerbate the global plastic problem. Filamentive research suggests that approximately 10% of 3D prints become waste. To quantify, if we assume there are currently, 232,000 3D printers installed in the UK and the average 3D printer (operator) uses 12 kg of filament annually – the estimated waste plastic generated by UK 3D printing users in 2021 can be inferred as 278,400 kg.

At the micro-scale, DIY recycling solutions exist – whilst this may be financially viable for businesses, it does remain expensive, labour-intensive and time-consuming for most. In a 2019 article exploring the sustainability of PLA, investment into large-scale bioplastic recycling was highlighted as a driver to increase recycling of PLA (3D printing) waste generally.

Pellet Extrusion 3D Printing

Fused Particle Fabrication / Fused Granular Fabrication (FPF / FGF) is an exciting development. Instead of filament, this extrusion system is enabled by plastic pellets, thus creating the potential for increasing recycled polymers in 3D printing. Such extrusion systems do not require the precise manufacturing tolerances compared to FFF extrusion, plus the technology is much faster, and reduces materials costs – producing filament (i.e. extrusion) is an added manufacturing step so working directly with pellets is advantageous. Whilst certainly a growing area, the FPF / FGF market is miniscule – currently <1% the size of the filament market, according to an industry insider.

Sustainability

Academic research has found that “material sustainability is an issue that can no longer be ignored due to wide adoption of 3D printing”.

In The State of 3D Printing Report: 2020 by Sculpteo, sustainability was identified as a key trend. Linked to this, a 2019 Filamentive survey found that:

- 97.5% of respondents consider plastic pollution a problem

- 99.5% of respondents believe it is important to behave sustainably

- 69% of respondents perceive the rise in plastic use in 3D printing to be a problem

Such findings exemplify that consumer awareness around sustainability has vastly increased in recent years and as seen in the results from this survey, it is clear that 3D printing users are extremely environmentally aware.

As concluded in a 2021 All3DP article, “adopting additive manufacturing and eco-friendly practices go hand in hand.” Reducing plastic waste is not only environmentally friendly, but a savvy business practice, too, as more consumers seek companies with sustainability principles.

Final Thoughts

With the rapid proliferation of FDM / FFF 3D printers making 3D printing technology affordable for both consumers and businesses alike, the market for plastic 3D printer filament in the UK will undoubtedly continue to grow, possibly worth in excess of £85m by 2024.

The use of plastic as a feedstock has the potential to exacerbate the global plastic problem. Generally, UK 3D printing users are certainly conscious of this and are increasingly looking for more sustainable options when it comes to their use of materials.

Whilst FPF / FGF technology may initially threaten the UK filament market, it may prove to be an opportunity for existing players and new start-ups alike – concurrently, increasing recycling and reducing 3D printing material costs for the end-user. Changes to the political and economic landscape due to Brexit could also be a catalyst for UK manufacturing of 3D printing filament.

With increasing adoption of bioplastics and recycled materials, we can reduce 3D printing’s reliance on (virgin) plastic, ensuring that as the UK 3D printing filament market grows substantially, it can also grow sustainably!

Filamentive (https://filamentive.com – [email protected]) is the market leader in sustainable materials for FFF 3D Printing. The company was founded to address the environmental need to use more recycled plastics in 3D printing, and also alleviate market concerns over quality and long-term sustainability. Filamentive has experienced rapid growth and continues to address the questions surrounding 3D printing recycled materials. Headquartered in Bradford, United Kingdom, its customers include a global network of makers, industry and education clients.